How Long Will Energy Prices Stay Depressed?

Natural-gas prices in March reached a new 10-year low, and they aren’t likely to go anywhere in a hurry. Record production of shale gas, coupled with the fourth-mildest winter on record, are keeping energy prices down.

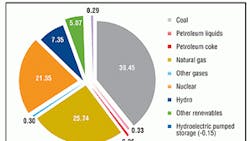

Consequently, electricity prices nationwide should remain relatively low as well. Since the 1990s, the percentage of total electricity produced from natural gas has risen gradually in the United States. Now, nearly 26 percent of electric generation in the country is fueled by natural gas (Figure 1). This number continues to rise as natural gas displaces coal for electricity generation. The relationship between coal, natural gas, and electricity can clearly be seen in Figure 2.

The Winter That Wasn’t

According to the National Oceanic Atmospheric Administration, since records began being kept in the 1890s only the winters of 1991-1992, 1998-1999, and 1999-2000 were warmer than this past heating season. The farther North and East you are in the country, the more evident this trend. While the Southwest was relatively normal, none of the lower 48 had a particularly harsh winter.

Fewer heating-degree days have left much of the country’s gas-storage capacity untapped. The U.S. Energy Information Administration claims America’s theoretical natural-gas storage capacity is 4.1 to 4.3 trillion cubic feet (tcf).

The injection period for natural gas is April through October. The winter withdrawal season is November through March. By the time the market walks out of withdrawal season at the end of this month, there may be more than 2.2 tcf remaining in storage—a level not seen since 1983. As a result of this surplus, the 2012 injection period should prove difficult for storage operators: where to put all the gas? This supply challenge is just one of several factors that could keep a lid on natural-gas prices for the balance of 2012.

In addition to supply headwinds, anemic demand in the United States also is unlikely to affect storage and pricing significantly. With manufacturing and natural-gas consumption closely linked, the likelihood of a dramatic price increase over last year is doubtful.

What Could Cause a Bull Market?

Although it’s likely the next year or two may see relatively low natural-gas prices, there are a number of factors that could disrupt this trend.

Gas producers in the Marcellus shale region claim a break-even price of $3.50 per dekatherm, while current market prices hover around $2.30 per dekatherm. As a result, many gas companies have started to cut production.

Recently, Chesapeake Energy, ConocoPhillips, Occidental Petroleum, EQT Energy, and Consol Energy (to name a few) have implemented production cuts in the Marcellus region. Chesapeake Energy led the way, announcing that it will immediately cut production by 0.5 billion cu ft per day and may increase this figure to 1 billion cu ft if pricing remains at “economically unattractive levels.”

Analysts agree that it could take months for a slowdown in drilling to translate to lower production. This is partially because of a shift in resources to higher-value oil and gas liquids which still produce plenty of associated gas. This is partially offsetting any reductions in dry-gas output. For example, natural gas is being flared off at many wet oil wells at the Bakken oil shale fields in North Dakota. Tightening supply may affect natural-gas prices over the next four to six months, which could bullishly impact electricity prices.

Unlike oil, natural gas doesn’t trade as a global commodity yet. The technology and processes used to convert natural gas from the ground into liquefied natural gas (LNG) are very costly and geographically challenging, which limits the ability to export the energy. Additionally, the regulatory hurdles to develop LNG facilities are massive. Many experts agree that it will be some time before the United States exports enough LNG to become a real factor in the global market.

Another influence that could play a large part in the price of natural gas in the future is how the United States capitalizes on the abundant resource. A massive overhaul of the U.S. transportation fleet from diesel—and to a lesser extent, gasoline—to CNG technology certainly would increase the demand for natural gas.

Without the fueling stations necessary to handle large quantities and widespread use of natural gas for transportation, a quick conversion will prove challenging. There has been some movement in that direction, however. Centre Area Transportation Authority (the bus line that serves the Pennsylvania State University main campus and surrounding areas) changed all of its primary buses to CNG, and Union Pacific awarded Amoco Corp. a supply contract for a blend of LNG to be used in the railroad’s LNG-locomotive test program. Conversions such as these can add some much-needed demand for this domestically abundant fuel.

Electric Volatility Remains

Currently, low natural-gas prices make for attractive electricity prices. However, as coal-to-natural-gas switching for electricity generation accelerates, the demand for natural gas may add support to pricing. As natural-gas prices rise, electricity prices may rise and start the migration back from natural gas to coal generation. In other words, many of the factors that impact natural-gas prices also will affect electricity prices, production cuts included.

In addition to production cuts, many nuclear plants cycle down for maintenance during the spring. Nuclear power accounts for about 20 percent of electricity generation in the United States, and when the plants go down, natural-gas-fired generation picks up the slack. This may have a bullish effect on natural-gas pricing, which may increase electricity-generation costs. Nuclear maintenance schedules in the spring also can provide early support for summer pricing. Nuclear plant outages as of March 2 were more than twice as high as they were last spring and more than 60 percent over the five-year average.

At the height of the spring 2012 maintenance season, more than 18,000 mw of nuclear power could be shut down nationally. It has been suggested that the increased number of outages this year are in response to the accident at the Fukushima nuclear power plant last year.

Adding fuel to the fire (pun intended), the U.S. Environmental Protection Agency finalized standards for toxic pollutants and mercury emission from coal-fired power plants in December. This could shut down or hamper electricity production from these plants. Although a federal appeals court issued an order delaying the Jan. 1 implementation, a reprieve may last only several months. The effects of this pending law have been felt throughout the country.

In the East, First Energy Corp., the nation’s largest investor-owned electric grid, announced in January that as a result of environmental regulations, it is closing six older coal-fired power plants in Ohio, Pennsylvania, and Maryland. As more coal-fired plants are forced to follow suit, it will have a bullish effect on natural gas and electricity pricing.

The Cycle Continues

Ultimately, the cure for low prices will be low prices. As discussed, natural-gas prices can affect many types of energy; however, prices can only fall in a straight line for so long before they trigger a bullish reaction in other markets. Natural-gas prices are trading at decade lows because of the increased production from shale plays, decreased industrial demand, and one of the warmest winters on record.

Extended low natural-gas prices have prompted producers to cap wells and encouraged coal-to-gas-switching for electricity generation. The longer this situation exists, the natural-gas supply-demand imbalance will improve slowly and prices will rise.

Enjoy the low prices while they last, but maintain your educational footing in transitory, minute-by-minute energy markets.

Tod W. Sherman is president and chief executive officer of Tybec Energy Management Specialists Inc. He has more than 15 years of energy-industry experience. He graduated from The Pennsylvania State University with a bachelor’s degree in civil engineering. Prior to founding Tybec with partners Doug Snyder and Mark Sahd, he worked in the regulated energy industry for UGI Utilities Inc. as an industrial and commercial sales representative and a distribution engineer. He also worked as a resident engineer in construction management, as well as a consulting civil engineer in Pennsylvania and Alaska.