Dodge Forecast: Industry Will Walk Tightrope in 2023

By ROB McMANAMY, HPAC Engineering

It was not lost on the online audience Nov. 15 that Dodge Construction Network Chief Economist Richard Branch was wearing a bow tie depicting flying pigs, as he delivered his 2023 industry forecast, entitled, "On the Razor’s Edge".

Branch laughed when one virtual attendee asked him about the tie, a gift from his wife, but its relevancy was clear. "Flying pigs" have long symbolized the impossible and the economist was suggesting that the U.S. economy could pull off the impossible next year. All it has to do is thread the needle between persistent inflation, rising interest rates and wages, resilient job growth and anxious building owners and developers, wondering if they should move forward on ample project backlogs.

Already, the U.S. economy has bounced back with growth in the third quarter of 2022 after two consecutive quarters of GDP decline, which used to be the definition of "recession." Still, the Federal Reserve Bank has been extraordinarily aggressive in trying to tame inflation, raising interest rates by 75-basis points on four different occasions this year, the latest announced Nov. 2. So far, that has brought the short-term borrowing rate into to a target range of 3.75%-4%, the highest level since January 2008.

Branch said Nov. 15, though, that he believes the Fed's aggressiveness has peaked. He predicts Fed Chair Jerome Powell will likely raise rates 50-basis points in December, and perhaps another 25 points apiece in both January and March of 2023. "But that should be it," said Branch. Even so, he also cautioned, "If we don't see core inflation improve, the Fed is going to keep fighting this battle. And I think they will win it eventually, but the Federal Reserve is not afraid to break the back of the economy to get us there."

But Branch does not think that will be necessary.

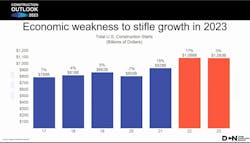

Overall, speaking as the main keynote for the 84th Annual Dodge Construction Outlook Conference, he predicted that total U.S. construction starts will be unchanged in 2023 at $1.08 trillion. When adjusted for inflation, total construction starts will dip 3%, he noted.

“As the clouds of uncertainty mount on the fate of the economy in 2023, the construction sector has already started to feel the impact of rising interest rates,” said Branch. "(And this) has raised concerns that a recession is imminent in the new year. Regardless of the label, the economy is slated to significantly slow, unemployment will edge higher, and for parts of the construction sector, it will feel like a recession.”

But Branch was also quick to add that whatever slowdown comes next year should not be anywhere near as severe as the one that hit it in 2008-2009.

“Next year, however, will not be a repeat of what the construction sector endured during the Great Recession when the financial system collapsed," he explained. "Residential construction, already reeling from rising mortgage rates, will continue to contract and will be joined by nonresidential construction as the commercial sector retrenches. (But) the funds provided to the construction industry through the Infrastructure Investment and Jobs Act (IIJA), The CHIPS and Science Act, and the Inflation Reduction Act (IRA) will counter the downturn allowing the construction to tread water."

Branch added, "During the Great Recession, there was no place to find solace in construction activity. 2023 will be quite different.”

Some key takeaways from the 2023 forecast:

- The dollar value of single-family starts will be flat (-5% when adjusted for inflation), however, units will be down a further 6% to 891,000 units (Dodge basis) as higher mortgage rates and worsening affordability eat away at demand;

- The multifamily sector has been reaping the benefits of the affordability issues plaguing the single family market, pushing demand for space up and vacancy rates down to record lows. The softening labor market and investment outlook will eat away at these gains in 2023. While the dollar value of multifamily starts will rise a scant 1% (-7% when adjusted for inflation), units will fall 9% to 723,000;

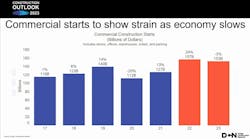

- Commercial starts will fall 3% in 2023 (-13% when adjusted for inflation) led by pullbacks in warehouse and office sectors. Hotel and retail starts will post tepid growth in nominal dollars, but when adjusted for inflation will also slip; but the declines will not be as dramatic as in office and warehouse. There is some positivity in the commercial space in 2023, though, as data center construction is expected to remain brisk;

- Institutional starts, meanwhile, will hold steady in 2023 (-1% inflation-adjusted) as gains in healthcare offset losses elsewhere. Traditional education starts (classrooms) have languished as slow demographic growth eats away at overall demand, however, life science buildings have flourished and will continue to do so in the new year. Healthcare starts will be the engine of growth in the institutional sector as greater demand for both outpatient clinics and hospitals is on the rise;

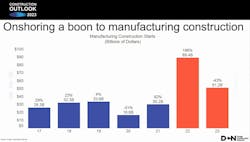

- Manufacturing starts have been robust since the pandemic as reshoring has led to numerous chip fabrication plants, EV battery plants, and other large facilities breaking ground. Manufacturing starts are expected to nearly triple in 2022, and while they will decline in 2023 the level of 2023 starts at $51 billion has not been seen since the beginning of Dodge’s historical starts time series in 1967. The CHIPS and IRA acts will support abnormally high levels of activity for years to come;

- Nonbuilding/infrastructure grouping of projects will be supported by an infusion of public dollars through IIJA. Public works starts will gain 18% in 2023 (+12% adjusted for inflation) led by gains in streets and bridge work, while the utility/gas category will gain 8% (+2% inflation-adjusted) as the extension of the investment and production tax credits in IRA will lead to gains in utility-scale wind and solar projects.

The day after the forecast conference, Dodge separately released its latest monthly construction starts data for October 2022, which rose 8% in October to a seasonally adjusted annual rate of $1.12 trillion. For the month, nonresidential building starts gained 9%, and nonbuilding starts rose 26%; however, as residential starts slipped 3%.

Year-to-date, total construction was 16% higher in the first ten months of 2022 compared to the same period of 2021. Nonresidential building starts rose 37% over the year, residential starts remained flat, and nonbuilding starts were up 17%.

“October’s gain in construction starts is a further sign that the construction sector continues to weather the storm of higher interest rates,” said Branch. “While the residential sector is feeling the pain, the nonresidential building and infrastructure sectors are hitting their stride.”

Of course, it remains to be seen how long those strides will last into 2023. But for now, Branch is relatively bullish about what's ahead. Provided the industry can continue to walk its tightrope.

#####

About the Author

Rob McManamy

Editor in Chief

An industry reporter and editor since 1987, McManamy joined HPAC Engineering in September 2017, after three years with BuiltWorlds.com, a Chicago-based media startup focused on tech innovation in the built environment. He has been covering design and construction issues for more than 30 years, having started at Engineering News-Record (ENR) in New York, before becoming its Midwest Bureau Chief in 1990. In 1998, McManamy was named Editor-in-Chief of Design-Build magazine, where he served for four years. He subsequently worked as an editor and freelance writer for Building Design + Construction and Public Works magazines.

A native of Bronx, NY, he is a graduate of both the University of Virginia, and The John Marshall Law School in Chicago.

Contact him at [email protected].