Architecture Billings Index Still Slow in February

PRESS RELEASE

WASHINGTON – March 22, 2023 – More architecture firms reported a decline in billings in February, indicating an extension of a recent downturn in design activity according to a new report released today from The American Institute of Architects (AIA).

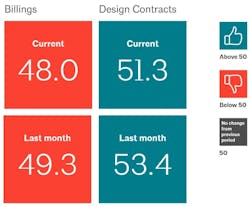

The score for February fell slightly to 48.0 (any score below 50 indicates a decline in firm billings). However, inquiries into new projects continued to improve, as did the value of new design contracts. Both indicators suggest that design work is expected to improve in the coming months.'

“The combination of an unsettled economy and high interest rates is causing investors and property owners to take a closer look at their plans for construction projects,” said AIA Chief Economist, Kermit Baker, Hon. AIA, PhD. “While this is producing delays for some projects under design, architecture firms are reporting that prospects for future project work remain generally positive.”

Key ABI highlights for February include:

- Regional averages: West (50.4); Midwest (48.8); Northeast (48.4); South (47.3)

- Sector index breakdown: mixed practice (57.0); institutional (46.9); commercial/industrial (45.8); multi-family residential (46.2)

- Project inquiries index: 55.0

- Design contracts index: 51.3

NOTE: The regional and sector categories are calculated as three-month moving averages and may not always average out to the national score.

- For more details about this, and past AIA reports, visit AIA’s website.

While overall billings have declined every month since October 2022, the pace of the decline remains relatively modest, and has not accelerated dramatically. This could potentially indicate a shorter slowdown at firms, rather than a more dramatic downturn and full-blown recession.

In addition, inquiries into new projects continued to grow at a steady pace this month, as did the value of new signed design contracts. Even while billings have slowed, there continues to be client interest in starting new projects.

Softness remained pervasive at firms across most of the country in February as well. Firms located in the West reported very minor growth, while firms located in all other regions saw declining billings. Conditions remained softest at firms located in the South for the third consecutive month. Billings also continued to decline at firms of all specializations this month.

The one exception is at firms with a mixed specialization, meaning that they do not receive 50% or more of their annual billings from any one of the three major sectors (multifamily residential, commercial/industrial, institutional). These firms have reported consistent growth every month for the last two years.

Despite economic concerns, companies continue to hire

In the broader economy, concerns about inflation and interest rates remain. The Consumer Price Index (CPI) indicated that inflation rose at an annual rate of 6.0% in February. While this is much better than it was a few months ago, it is still about double the Federal Reserve’s target rate.

Because of that, it seems likely that the Federal Reserve will raise interest rates by another 0.25 percentage points at their meeting later this month, unless they decide to temporarily pause the increases due to the fallout from the recent failures of Silicon Valley Bank and Signature Bank. (UPDATE: The Fed did raise rates by a quarter point on March 22.)

However, companies are largely still hiring more employees, with nonfarm payroll employment adding another 311,000 new jobs in February, and construction employment contributing 24,000 of those positions. Architectural services employment has flattened in recent months, declining by 400 positions in January (the most recent data available), for a combined loss of 600 jobs since its most recent peak in November 2022.

Recruitment, compensation top of mind for firm leaders

For this month’s special topical questions, we asked firm leaders about recent issues related to architectural staff compensation at their firm. Overall, 86% of responding firm leaders indicated that recruiting new architectural staff is currently an issue at their firm, with 62% indicating that it is a major issue. In addition, 83% of firm leaders reported that meeting future staff compensation expectations was an issue, with 47% indicating that it is a major issue.

Firm leaders also generally believe that architectural compensation is the most serious of an issue for mid-level architectural staff with four to 10 years of experience, with 36% indicating such. And about 16% of firm leaders reported that they find that compensation is the most serious of an issue for senior level architectural staff (10+ years’ experience), 14% find it to be the most serious of an issue for entry level staff (less than four years’ experience), while the remainder indicated that it’s about equal for all staff levels. Small firms were more likely than other firms to be concerned about compensation for senior level staff.

Firms also reported that compensation levels for architectural staff at their firm increased by an average of 6.8% from 2021 to 2022. Large firms (7.3%), and firms located in the West (7.3%) and Midwest (7.0%), tended to report larger increases. Overall, 90% of firms indicated that salaries for architectural staff at their firm increased in 2022, while 8% indicated that they remained at the same level as 2021, and just 2% saw declining salaries. However, 11% of firms with annual billings of less than $250,000, and 6% of firms with annual billings of $250,000 to $1 million, saw declining compensation in 2022.

Looking forward to 2023, 83% of firms expect further increases in architectural staff compensation, with average growth leveling out at about 4.0%. Just under 15% of firms expect compensation levels to remain the same as in 2022, and 2% expect a decrease. Larger firms generally predict higher compensation growth than small firms (4.4% for firms with annual billings of more than $5 million versus 1.8% growth at firm with annual billings of less than $250,000), while firms located in the South are expecting smaller increases (3.5% on average).

NOTE: The new 2023 AIA Compensation & Benefits Survey Report will be released this summer.

This month, Work-on-the-Boards participants are saying:

- “Slightly declining on the whole. We’re working harder to maintain backlog and workload.”— 45-person firm in the Northeast, residential specialization

- “We are shifting from several large, complex projects to many smaller, market-focused projects requiring high degrees of collaboration and coordination to deliver under tight deadlines.”—120-person firm in the South, institutional specialization

- “Business conditions are good, but hiring additional staff is still so difficult that it’s hard to grow the firm.”—132-person firm in the Midwest, commercial/industrial specialization

- “We had a few large, multifamily projects go on hold in the last four months and had to lay off 10% of our staff.”—32-person firm in the West, mixed specialization

For more, contact Tim Trudell at AIA, [email protected].