AIA: Demand for Design Services Up Again in November

PRESS RELEASE

WASHINGTON – Dec. 15, 2021 – Architecture firms reported increasing demand for design services for the 10th consecutive month in November, according to a new report today from The American Institute of Architects (AIA).

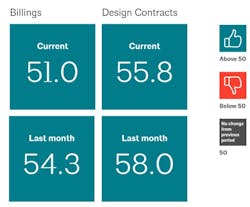

The ABI score for November was 51.0, down from 54.3 the previous month. While this score is down slightly from October’s score, it still indicates positive business conditions overall (any score above 50 indicates billings growth). During November, scoring for both the new project inquiries and design contracts moderated slightly, but remained in positive territory, posting scores of 59.4 and 55.8 respectively.

“The period of elevated billing scores nationally, and across the major regions and construction sectors seems to be winding down for this cycle,” said AIA Chief Economist, Kermit Baker, Hon. AIA, PhD. “Ongoing external challenges like labor shortages, supply chain disruptions, spiking inflation, and prospects for rising interest rates will likely continue to slow the growth in firm billings in the coming months.”

Baker noted that a growth rate like what was experienced this past spring and summer is difficult to maintain for long, and firm billings have now shifted closer to the pace of growth seen in previous recovery periods. In addition, firms continue to report a very strong amount of work in the pipeline, with inquiries and the value of new design contracts remaining near all-time high levels.

However, business conditions did slide further in November at firms located in the Northeast, marking the third month in a row of declining billings. Conditions in the Northeast have been up and down over the last several years, even prior to the pandemic, and it appears that trend is continuing now.

On the other hand, billings in other regions of the country remain fairly strong, particularly at firms located in the Midwest, where the highest scores have generally been reported during this most recent recovery period. Firms of all specializations also reported improving business conditions in November, although the pace of growth did slip for all. Business conditions remain strongest at firms with a multifamily residential specialization, although it seems like that market may be slowing somewhat now too.

Supply chain disruptions and labor shortages continue to cause constraints

The latest issue of the Federal Reserve’s Beige Book report, released on December 1, indicates that the broader US economy grew at a modest to moderate pace in the October-November period. Despite relatively strong growth in the economy overall, supply chain disruptions and labor shortages have continued to cause major constraints, with construction activity being one of the most-affected sectors. Hiring issues are widespread as well, with companies offering higher wages and increasing other incentives to entice potential employees. Manufacturing growth was also solid during this time period, and nonresidential real estate activity increased, but residential real estate activity was more mixed.

Nonfarm payroll employment grew by 210,000 positions in November, significantly below the average monthly gains of 555,000 for the year so far, as overall national employment remains 2.6% below its pre-pandemic peak. Construction employment continued to rise, adding another 31,000 jobs in November, with 10,000 of those from the construction of buildings. And the architectural services sector continues to surpass its pre-pandemic peak, adding another 1,600 new jobs in October (the most recent data available), rising to a total of 200,900 employees in the industry. A total of 17,700 new jobs have been added since the low point in July 2020 during the COVID-induced recession.

Top Issue for 2022: Firm profitability

This month, we asked survey panelists about their biggest business-related concerns for 2022. As in most years, these concerns largely revolved around issues related to firm and project management, as well as staffing. Many of the top issues from last year that related to remote work and uncertainty due to the pandemic fell off the top ten list this year, replaced by concerns about hiring and retaining staff.

The number one issue for 2022 remains the perennial concern about increasing firm profitability, with more than one quarter of responding firms (27%) selecting it as one of their top three concerns for the coming year. The second highest rated concern has to do with coping with volatile construction/building materials costs and availability, which was cited as a top concern by 24% of firms and has been an issue throughout much of this year. That now looks to carry into the new year as well.

The primary issue related to staffing in 2022 is expected to be finding candidates to fill key positions at firms, which 22% of firms rated as one of their top three issues, as well as more generally filling open staff positions (19%), retaining current staff (16%), and maintaining competitive salaries/dealing with staff compensation expectations (10%). These issues also tie into concerns about firm ownership transition issues (21%), and even concerns about negotiating appropriate project fees (14%), as several respondents indicated that they may need to adjust their fees to meet increased compensation and benefits needs of incoming new hires.

Overall though, the majority of responding firms (78%), expect that 2022 will be a good to great year for their firm, with just 11% expecting it to be challenging or disastrous. Firms located in the Northeast were most likely to report expecting a harder time next year, with 20% expecting it to be challenging, while large firms with annual billings over $5 million were most likely to expect to have a good to great year (87%).

This month, Work-on-the-Boards participants are saying:

- “There is tremendous backlog building going into 2022, but limited availability of new staff to do the work.”—185-person firm in the Midwest, residential specialization;

- “Things have been busy. It is hard to gauge how strong things will stay into later next year. Materials shortages and costs are also very impactful.”—1-person firm in the Northeast, commercial/industrial specialization;

- “We have a tremendous number of RFQ’s in the past 30 days. If we can land one or two our year will move up to great.”—6-person firm in the West, institutional specialization;

- “2021 has been a busy and somewhat surprisingly good year. However, with the uncertainty around the increase in inflation and the emergence of the omicron variant, 2022 is a bit of a puzzle in spite of a currently strong backlog.”— 65-person firm in the South, institutional specialization.

##########

CONTACTMatt Tinder(202) 626 7462[email protected]