AIA: Billings Index Ends 2021 on High Note as Firms Seek More Staff

PRESS RELEASE -- AMERICAN INSTITUTE OF ARCHITECTS

WASHINGTON – Jan. 19, 2021 – As architecture firms ended 2021 on a high note with strong business conditions, staff recruitment is becoming a growing concern among many.

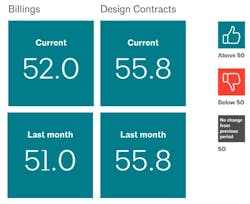

December’s Architectural Billings Index (ABI) score of 52.0 was an increase from 51.0 in November (any score over 50 indicates billings growth). Despite a variety of concerns related to the Omicron variant, labor shortages, and rising prices as well as limited availability of construction materials, firms continued to report a robust supply of work in the pipeline. Inquiries into new work and the value of new design contracts both remained strong, and backlogs, at an average of 6.5 months, remained near their highest levels since the AIA began tracking this metric in 2010.

“Since demand for design projects has been healthy over the last year, recruiting architectural staff to keep up with project workloads has been a growing concern for firms,” said AIA Chief Economist, Kermit Baker, Hon. AIA, PhD. “Architecture is one of the few industries where payrolls have already surpassed their pre-pandemic high, so meeting future staffing needs is a challenge that most firms will need to confront."

Recruiting architecture staff to meet workloads is a concern at most firms

Business conditions at architecture firms ended 2021 on a high note, with an Architecture Billings Index (ABI) score of 52.0 in December (any score over 50 indicates billings growth). Firm billings increased every month of the year except for January, as most firms experienced a strong rebound from the 2020 downturn. And despite a variety of concerns related to the omicron variant; prices/availability of construction materials; and labor shortages, firms also continued to report a robust supply of work in the pipeline, with inquiries into new work and the value of new design contracts both remaining strong, and backlogs remaining near the highest levels ever reported since we started collecting this data in 2010, at an average of 6.5 months.

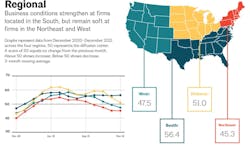

End-of-year conditions vary by region and specialty

Business conditions were more variable by both region of the country and firm specialization in December. Firms located in the Northeast experienced their fourth consecutive month of declining billings, while firms located in the West saw billings decrease for the second month in a row. Firms located in the Midwest and South continued to report an increase in billings, but the pace of growth has slowed substantially at firms in the Midwest in recent months. Only firms located in the South have continued to report a consistently high level of billings recently.

However, firms of all specialization reported a decline in firm billings in December, with only those with a mixed specialization (defined as those firms not having at least 50% of their billings in one of the other three categories: multifamily residential, commercial/industrial, or institutional) experiencing growth. Even firms with a multifamily residential specialization experienced a decline in billings for the first time in nearly a year, while firms with an institutional specialization reported their second straight month of softness. There is always some softness in firm billings at the end of the year, due to the holiday season and colder weather, but seasonal adjustment of the data typically smooths much of that out. But because of that, it is too early to say whether this is just a seasonal blip, or the start of a more concerning trend.

Employment growth continues through December

In the broader economy, nonfarm payroll employment added 199,000 new positions in December, with total national payrolls now just 2.3% below their pre-pandemic peak. Construction employment added an additional 22,000 jobs in December as well, notably with 13,000 in nonresidential specialty trade contractors. And architectural services employment added an additional 100 jobs in November, the most recent data available, for a total of 11,000 jobs added through the first 11 months of 2021.

Staff recruitment continues to be key concern for firms

As mentioned above, staffing has been an issue of increasing concern for many firms in recent months, with one in five firms reporting staffing issues as a key concern for 2022 in last month’s survey. This month we asked firms more specifically about the seriousness of the issue, and the actions that they have taken to recruit and retain staff.

Overall, firms are more concerned about recruiting architectural staff at their firm than retaining architectural staff, with 42% of responding firms indicating that recruiting architectural staff is a very serious problem at their firm, in contrast to just 14% who said the same about retaining architectural staff at their firm. In addition, 40% of firms said that recruiting staff is somewhat of a serious problem, while 18% said that it is not a problem.

On the other hand, 42% of firms said that retaining staff was not a problem, and 44% said that it was somewhat of a problem. Firms located in the South, where business conditions have been strongest recently, were most likely to report having a serious problem with recruiting staff (48%), versus just 36% of firms located in the Northeast. Large firms were also more likely to report having a problem recruiting staff, as were firms with an institutional specialization.

Given anticipated project workloads over the coming months, more than eight in 10 responding firms indicated that they are at least somewhat concerned about being able to recruit and retain staff, with 27% indicating that they are quite concerned, and 10% indicating that they are very concerned.

Once again, firms located in the South, as well as large firms, and those with an institutional specialization, were most likely to report a higher degree of concern about being able to recruit and retain enough staff to meet upcoming workloads.

When asked about what actions they have already taken in relation to current architectural staffing conditions, 90% of responding firms indicated that they have taken at least one action, with nearly half (49%) reporting that they have Increased salaries above typical levels to retain current staff. An additional 45% reported that they have offered additional employee perks (e.g., 4-day work week; ability to work remotely), while 39% have increased salary offerings above typical levels to attract qualified candidates. Firms have also made some project-related changes, with 31% indicating that they are not bidding on projects that their firm is otherwise qualified to handle due to staffing shortages, and 30% are extending/delaying project schedules on existing projects. Just under one quarter of firms (24%) have hired contract workers, but few have outsourced work either domestically or offshore.

However, of the steps that firms have not yet taken, one in five (21%) would consider hiring contract workers if the staffing situation becomes more serious in the coming months, and 18% would consider outsourcing work to other domestic firms. In addition, 20% would choose to not bid on projects that their firm is otherwise qualified to handle, 19% would extend/delay project schedules on existing projects, and 16% would increase firm revenue to help cover additional staff compensation costs. Fewer firms would make changes to current staff salaries/benefits, but that is because most of the firms that would make that change have already done so.

Finally, when asked about the effectiveness of making these changes to address staffing issues at their firm, most firms rated issues related to increasing staff and potential staff salaries, and offering additional employee perks and benefits, among the top three most effective changes that they have/could make, followed by making changes to projects/project schedules and hiring new employees/outsourcing work.

This month, Work-on-the-Boards participants are saying:

- “Very competitive for the projects that are out there.”—45-person firm in the Northeast, residential specialization;

- “Business conditions remain strong. There is cash available locally for private sector work to move forward and the low interest rates are very attractive to that segment of our clientele.”—8-person firm in the West, institutional specialization;

- “Continue strong, but Covid is affecting attendance at several of our clients’ offices and on our jobsites.”—8-person firm in the South, commercial/industrial specialization;

- “Typical mid-November through first of the new year slowdown regarding new inquiries and awards.”— 2-person firm in the Midwest, mixed specialization.

##########