AIA: Demand For Design Services Slowing

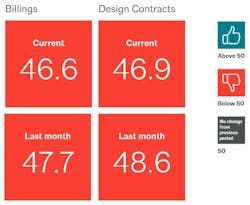

WASHINGTON – Dec. 14, 2022 – After U.S. architecture firms experienced their first decline in billings in nearly two years in October, business conditions softened further in November, as the American Institute of Architects' monthly Architecture Billings Index (ABI) score fell to 46.6 (any score below 50 indicates a decline in firm billings).

While inquiries into new projects continued to rise modestly, the value of new design contracts also dropped further in November. This indicates that not only are firms seeing a decline in current work, but that less new work is entering the pipeline, as well.

The pace of inquiries into new projects slowed, but remained positive with a score of 52.0. However new design contracts remained in negative territory with a score of 46.9.

“Given the slowdown in new project work, many architecture firms will rely on their near record levels of backlogs to support revenue,” said AIA Chief Economist, Kermit Baker, Hon. AIA, PhD. “Still, firm leaders remain largely optimistic about future business trends. Almost two-thirds of architecture firms project that 2023 will be either a good year or great year for their firm.”

__________

Key ABI highlights for November include:

- Regional averages: South (50.5); Midwest (47.6); West (45.8); Northeast (42.4)

- Sector index breakdown: mixed practice (51.5); institutional (47.7); multi-family residential (46.1); commercial/industrial (44.2).

NOTE: The regional and sector categories are calculated as a three-month moving average, whereas the national index, design contracts and inquiries are monthly numbers.

_________

In Novermber, business conditions softened in nearly all regions of the country. Only firms located in the South, which has seen some of the strongest growth throughout the post-pandemic period, reported a small increase in billings. Firms in the Northeast have seen the largest decline in billings so far, and only experienced a few months of growth earlier this year before returning to negative territory. Firms of all specializations also saw weaker business conditions this month, including those with an institutional specialization, where conditions had been fairly robust recently.

Rising interest rates continue to flatten economy

In the broader economy, there are signs of concern as well. In the most recent edition of the Federal Reserve’s Beige Book report, released on November 30 and covering conditions in the previous six weeks, economic activity was reported as being largely flat across much of the country, or expanding with a slower pace of growth than in recent months. In addition, there was more pessimism about the overall economic outlook, given the ongoing impact of inflation and higher interest rates.

In particular, interest rates had a large impact on home sales in areas like Atlanta, St. Louis, Dallas, and San Francisco. Both residential and nonresidential construction declined in most areas, although nonresidential construction declined at a slower pace. In addition, tightening credit standards have led to declines in bank lending, which may also have an impact on construction in the coming months.

However, companies are largely still hiring. Nonfarm payroll employment added an additional 263,000 new jobs in November, and construction employment grew by 20,000 employees, 8,000 of which were hired for nonresidential building construction. However, architecture services sector employment declined for the second month in a row in October (the most recent data available), shedding an additional 300 positions, for a total decline of 800 positions over the last two months.

Despite declines, firm leaders remain optimistic

This month, AIA asked firm leaders about their expectations and concerns for the coming year. Despite the recent downturn in billings, firm leaders remained largely optimistic about 2023, with 63% expecting it to be a good to great year for their firm. Just 16% expect it to be a challenging or disastrous year, while 21% think that it will be a more mixed, or so-so year.

However, some firms were more concerned. One quarter of firms located in the Northeast, and 25% of firms with annual billings of less than $1 million, expect 2023 to be challenging or disastrous. On the other hand, 68% of firms located in the Midwest, and 70% of firms with annual billings of $1 million or more, expect a good or great year next year.

The overall list of the top business concerns for the coming year for architecture firms is largely the same for 2023 as it was for 2022.

Coping with volatile construction/building materials costs and availability and increasing firm profitability remained the top two issues, selected by 26% and 25% of responding firms, respectively. Increasing profitability is almost always one of the top concerns for firm leaders, regardless of what else is occurring in the economy at that time. Following those two concerns are ones about staffing: 20% indicated that finding candidates to fill key positions at their firm is one of their biggest concerns for 2023, while 17% selected filling open staff positions, and 10% selected retaining current staff.

Issues related to running their firm were also high on the list, notably dealing with ownership transition issues, and managing the cost of running the firm/maintaining competitive salaries. And while 48% of responding firm leaders indicated that increasing the long-term commitment of younger staff to the profession is a major issue, just 6% selected it as one of their top concerns for 2023.

While there were some firms that indicated that issues like increasing firm work on existing buildings and implementing new project delivery methods are a major concern at their firm for the coming year, fewer than 1% of respondents selected those issues as one of their top concerns for the coming year.

In addition, more than 60% of respondents indicated that issues like managing possible merger and acquisition activity and managing a portion of the workforce that stays remote permanently are not a concern at all at their firms.

AIA Work-on-the-Boards participants are saying:

- “The last four months have seen a significant slowdown in the amount of proposals for significant healthcare projects. Many existing projects are plagued by cost increases and have slowed down or been put on hold until additional funding is secured.”—120-person firm in the Northeast, institutional specialization;

- “Planning approvals and environmental reviews, along with protracted plan check reviews by building departments, are stretching project schedules, leading to hesitancy by some clients to start construction. This makes office workflows and staffing very challenging”— 12-person firm in the West, commercial/industrial specialization;

- “Business conditions are showing some signs of fraying around the edges. Clients have taken a bit more coaxing to pay their bills. Project budgets and certainty are being called into question.”—45-person firm in the Midwest, institutional specialization;

- “Metro Atlanta is very busy, and while the housing market will take a hit, there are many other sectors that will continue to thrive.”— 15-person firm in the South, mixed specialization.

For more ABI monthly reports, click here.