Shale-Gas Production Trumps Market Disrupters

If you are planning an HVAC-system retrofit for a customer this summer, your life-cycle analyses will have one more constant than in years past: the price of natural gas. Building owners and equipment specifiers can be confident the price of natural gas will most likely remain stable throughout the life of newly installed equipment.

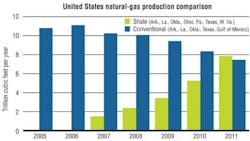

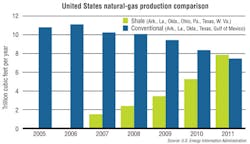

Until recently, the majority of the nation’s natural gas has come from traditional wells in and around the Gulf of Mexico, which meant hurricanes and tropical storms had the capacity to create major disruptions in gas price and supply. However, in 2011, natural-gas production from conventional sources in the Gulf region was surpassed by deep shale plays in states across the country (Figure 1).

Severe weather events in the Gulf region affect gas supply and prices in two ways.

First, in anticipation of a storm, offshore platforms are shut down. Crews secure and evacuate the facility and do not return until the weather event has dissipated. A minimum of two weeks is lost during this process. We saw this in the wake of hurricanes Katrina and Rita, the Class 5 storms that one-two punched U.S. natural-gas prices in 2005.

According to the U.S. Energy Information Administration (EIA), more than 800 offshore platforms were evacuated in the Gulf of Mexico during Hurricane Katrina. In the case of Hurricane Rita, all 4,000 platforms were evacuated. Additionally, onshore wells in the Gulf region were secured and evacuated in preparation for the hurricanes.

Second, damage to the actual processing and gathering infrastructure has a lasting impact on the market. During Katrina and Rita, 111 Gulf platforms were destroyed. This number does not even address the damage sustained by gas processors, pipelines, and on-shore storage facilities.

In response to these two hurricanes, gas prices jumped from $8 per million British thermal units in August 2005 to more than $12 per million British thermal units in October. A year later, the price had fallen below $6 per million British thermal units.

Fracking and Shale Production Stabilizes the Market

As Figure 1 illustrates, 2011 was the first year that natural-gas shale production across the nation surpassed that of conventional withdrawals. Despite environmental opposition, modern horizontal fracking technologies have insulated end-users from Mother Nature’s wrath with historically low and stable prices.

States that historically had limited capacity to withdraw natural gas from conventional wells have found a sustainable opportunity with horizontal fracking. Additionally, states that were limited to conventional means of production in the past have expanded their output through fracking. This phenomenon is most evident in the Marcellus shale region in the Northeast, the Haynesville and Eagle Ford regions in the South, and the Bakken region in the Midwest. However, shale production and exploration have popped up in other areas, such as California and Florida, as well. Other states—New York, for example—are on the brink, pending state legislation.

For the first time, more gas is coming from shale deposits across the country than conventional wells in the Gulf region. This means less fluctuation in supply and more dependable gas prices in the years to come. With such stability, lifetime cost projections in heating- and process-equipment investments are more predictable than in the past.

There are a few demand considerations that could provide headwinds to price stability in the future. The most likely scenario, which was seen last spring and summer, is the increased demand by electric utilities for natural-gas-fired generation vs. coal. Although natural-gas was cheaper than coal, the percentage of natural gas used for electric generation in 2012 increased from just over 26 percent in January to just below 33 percent in April.

In contrast, coal’s percentage of electric generation fell from 38 percent in January 2012 to just below 33 percent in April 2012. This was the first time the EIA had reported equal generation usage for both fuels since it began compiling the statistics.

Additionally, if technology, investments, and government regulations evolve to readily export natural gas, it could become an extremely valuable commodity on the international market. Right now, the export and transportation of natural gas via liquefied-natural-gas terminals is costly and mired in red tape. Even further down the road, a push to use compressed natural gas for domestic transportation (mainly fleets) would have the potential to increase demand and prices.

Considering none of these scenarios would occur overnight, supply should have plenty of time to meet the higher demand. Natural-gas reserves in the United States are vast, and all signs point to sustained affordability for the foreseeable future.