Tales of Two Industrial Trends Converge on 2022

The relentless push and pull of this exhausting last year continues to remind us daily that nothing is ever easy in our pandemic-altered world. This spring, as the number of fully vaccinated Americans has surged past 100 million citizens, federal stimulus dollars have continued to flow, and the Centers for Disease Control has relaxed certain outdoor mask guidelines in the U.S., alarming health news from India continues to keep the rest of the globe on edge.

Similarly, even as the U.S. construction industry has begun to exhibit more strength, now materials shortages and price increases are threatening the rebound. Total U.S. construction starts rose 2% in March to a seasonally adjusted annual rate of $825.3 billion, according to the latest Dodge Data & Analytics report, relreased April 16. A solid gain in nonresidential building starts fueled the growth, but the rise was not without caveats.

“The March increase in construction starts is certainly welcome news following the past three months of decline,” said Richard Branch, Chief Economist for Dodge Data. “Construction will continue to improve as the year moves on. However, just as the pandemic is beginning to loosen its grip on the economy, logistical problems and the rapid escalation in material prices have stepped in as the primary risk to the construction sector. These issues may restrain opportunity in the coming months, causing the sector’s recovery to lag that of the overall economy.”

Indeed, the overall U.S. economy grew at a 6.4% annualized rate during the first quarter of 2021, according to the April 29 report from the Bureau of Economic Analysis at the U.S. Dept. of Commerce. “The U.S. economy expanded rapidly during the quarter, but investment in nonresidential structures actually subtracted from growth,” noted Anirban Basu, chief economist at Associated Builders and Contractors (ABC). “The COVID-19 pandemic leaves in its wake low hotel occupancy rates, vacated offices, and large blocks of abandoned retail space," added Basu. "(But) the expectation for rapid economic growth into 2022 remains firmly in place,” he added.

Such seemingly contradictory evidence is especially prominent in the industrial and manufacturing market, where analysts reported a significant slowdown in new factory construction last year. At the same time, however, warehouse projects took off as e-commerce soared during the pandemic.

Indeed, as we reported in our December 2020 cover story, retail giant Amazon even accelerated its expansion plans to lead an extraordinary building boom of massive fulfillment centers across the U.S., each in the range of 800,000-sq-ft and located near transportation hubs. Overall, at least 20 such centers were expected to come on line in 16 states, most by the middle of 2021. But others are just getting started.

In fact, in March, Dodge Data says the two largest nonresidential building projects to break ground in the U.S. were both industrial: a $306-million Amazon warehouse in Maspeth NY, and a $300-million Ball Corp. Aluminum Can factory in Pittson PA. Ball also is building plants this year in Glendale AZ and Bowling Green KY.

This week, another large industrial project entered the market when Toyota Motor Corp. announced April 28 that it will invest $803 million to expand existing manufacturing facilities in Princeton, IN.

According to the latest AIA Consensus Construction Forecast for 2021, released in December, the roughly $71-billion U.S. industrial construction market was expected to slip 4.5% overall this year, before bouncing back 1.5% in 2022. Combining predictions from the American Institute of Architects and eight other economists, the consensus forecast for next year would have been much more optimistic save for the one outlier, Dodge Data.

- To view the interactive AIA chart, click here.

Among the individual forecasters, Dodge predicted that new contracts for the industrial sector would plummet 17.5% by the end of this year, and fall another 15.5% next year. But the other firms all forecast gains for 2022. ABC even predicted a rise for this year. Respectively, here is what they expect for the industrial market:

- Moody's Analytics >> 2021: -3.4; 2022: +5.9%;

- IHS Economics >> 2021: -5.8%; 2022: +3.4%;

- ConstructConnect >> 2021: -3.3; 2022: +2.4%;

- Wells Fargo Securities >> 2021: -3.5; 2022: +3.2%;

- Markstein Advisors >> 2021: -4.1%; 2022: +4.7%;

- Associated Builders & Contractors >> 2021: +6.5; 2022: +3.7%;

- FMI Corp. >> 2021: -5.0%; 2022: +5.0%.

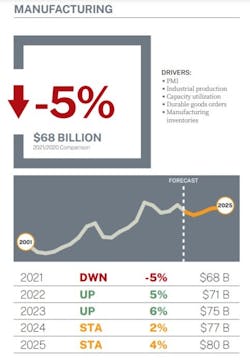

FMI also released a more detailed analysis of its own for the U.S. manufacturing market, logging predictions all the way out through 2025. In its latest Q2 Outlook Report for 2021, the firm says it expects to see the overall size of the U.S. market climb from $68 billion in 2020 to $80 billion in 2025. To get there, FMI foresees four consecutive years of annual increases, starting in 2022.

- Supply chain constraints (e.g., lumber, semiconductors, etc.) are expected to remain in place well into 2021 as the global economy rebounds and international trade negotiations resume;

- Oil-related demand disruptions continue to weigh on manufacturing investment across chemical and refining operations well into 2021;

- Spending growth returns in 2022 as owners pursue modernization investments and resume expansion.

OWNERS' PERSPECTIVE POSITIVE

On March 9, the National Association of Manufacturers (NAM) released its first members Outlook Survey of 2021, and the first since the new Biden Administration took office. Based on 450 member responses, the survey showed manufacturers’ optimism increasing to nearly 88%—the highest reading in two years, and up from 74% in the Q4 2020 survey. This steady improvement represents an increase of 54 percentage points since the results of the first survey that measured manufacturers’ sentiment after the pandemic was declared (34% in Q2 2020).

“As vaccines roll out at a faster pace and we see signs of an improving economy, manufacturers’ optimism is rising fast,” said NAM President and CEO Jay Timmons. “Our industry is creating new jobs and investing in new projects, buoyed by signs that we may finally be getting COVID-19 under control. Of course, our industry knows we are not out of the woods yet. That’s why we continue to lead by example, wearing face coverings and promoting vaccination. The smart health protocols are more important than ever. This is our shot—not just to end the pandemic but to build a new and stronger economy that creates opportunity for all.”

Of particular note, capital spending expectations were the strongest in two years, with respondents anticipating an average increase of 2.7% over the next 12 months, up from the 1.5% prediction recorded in the fourth quarter of 2020. In this NAM survey, almost half of those responding also said that they expect additional capital spending in the next year, with 38.9% expecting no change and 11.3% forecasting reduced capital expenditures. By firm size, small, medium and large manufacturers said they foresee capital spending increasing 1.3%, 3.0% and 3.2%, respectively.

Good signs for the industrial construction market, from those who will be awarding the contracts.

Looking at the broader market, ABC's Basu this week added, “While many fret about input shortages, rising inflationary pressures, prospective tax increases and skyrocketing national debt, for now the sheer volume of federal spending will countervail all headwinds. Employment growth will be significant for months to come, which will help support commercial real estate fundamentals and eventually produce a rebound in commercial construction. Recent upticks in contractor confidence, according to ABC’s Construction Confidence Index, all support this notion."

##########

About the Author

Rob McManamy

Editor in Chief

An industry reporter and editor since 1987, McManamy joined HPAC Engineering in September 2017, after three years with BuiltWorlds.com, a Chicago-based media startup focused on tech innovation in the built environment. He has been covering design and construction issues for more than 30 years, having started at Engineering News-Record (ENR) in New York, before becoming its Midwest Bureau Chief in 1990. In 1998, McManamy was named Editor-in-Chief of Design-Build magazine, where he served for four years. He subsequently worked as an editor and freelance writer for Building Design + Construction and Public Works magazines.

A native of Bronx, NY, he is a graduate of both the University of Virginia, and The John Marshall Law School in Chicago.

Contact him at [email protected].