LABOR DAZED: Construction Employment Dips, Demand Frustrated

Just weeks ago, this monthly economic pulse check was bouyed by the looming passage of a $1-trillion federal infrastructure bill, which eventually cleared the U.S. Senate by a bipartisan vote of 69-30 on Aug. 11. Indeed, broad economic stimulus truly seemed to be at hand.

But now, as Labor Day arrives, final passage of a reconciled House-Senate version of that vital legislation remains unfinished and now will not even be voted on in the roiling U.S. House of Representatives until Sept. 27, at the earliest.

So, nationwide anxiety is back, unfortunately, fueled by multiple factors.

The latest evidence arrived Sept. 3, when the U.S. Bureau of Labor Statistics (BLS) delivered an unexpectedly underwhelming jobs report for August. For the month, the economy added 235,000 positions, well below the 720,000 figure that economists surveyed by Dow Jones had recently predicted. Even so, President Biden noted Sept. 4 that the latest gains still represented the eighth straight month of positive job growth since December's net loss of more than 300,000.

For its part, the construction industry lost 3,000 jobs on net in August, according to an Associated Builders and Contractors analysis of the BLS data. Despite the monthly setback, the industry has recovered 881,000 (79.2%) of the jobs lost during earlier stages of the pandemic.

Nonresidential construction employment declined by 20,300 positions on net, but overall, the construction unemployment rate fell sharply to 4.6% in August, down from 6.1% in July. Overall, unemployment across all industries declined from 5.4% in July to 5.2% last month.

“While the ongoing pandemic clearly had an impact on employment in segments such as retail, lodging and restaurants in August by suppressing demand for additional workers, construction employment dynamics were more affected by ongoing supply-side bottlenecks," said ABC Chief Economist Anirban Basu. “Collectively, nonresidential contractors exhibited significant confidence in the past few months, but in general, positive expectations have gone unmet, at least thus far. Industry participants had anticipated rising employment during the back half of 2021, according to ABC’s Construction Confidence Index, but nonresidential employment declined by more than 20,000 positions in August. Anecdotal evidence suggests that many projects have been put on hold. This is due to lofty construction costs, which is the result of global supply chains in disarray and growing difficulty hiring skilled construction workers."

Indeed, those factors were underscored Sept. 2 with the release of a new workforce survey conducted jointly by the Associated General Contractors of America (AGC) and Autodesk. The survey results found construction firms struggling to find enough qualified workers to hire even as they continue to be impacted by pandemic-induced project delays and supply chain disruptions. So, the pandemic has created constraints on the demand for work even as it limits the number of workers available to hire.

“Market conditions are nowhere near as robust as they were prior to the onset of the pandemic,” said Ken Simonson, AGC’s chief economist. “At the same time, the pandemic and political responses to it are limiting the size of the workforce, leading to labor shortages that are as severe as they were in 2019 when demand for construction was more robust.”

Of note, the AGC-Autodesk Workforce Survey was conducted in late July and early August. Over 2,100 firms completed the survey from a broad cross-section of the construction industry, including union and open shop firms of all sizes. The 2021 Workforce Survey is the association’s ninth annual workforce-related survey.

Simonson noted that nearly nine out of ten firms (88 percent) are experiencing project delays. Among these firms, 75 percent cite delays due to longer lead times or shortages of materials, while 57 percent cite delivery delays. Sixty-one percent of firms said their projects are being delayed because of workforce shortages. And delays due to the lack of approvals or inspectors, or an owner’s directive to halt or redesign a project, were each cited by 30 percent of contractors.

An even higher percentage of firms, 93 percent, report that rising materials costs have affected their projects. These rising materials costs are undermining firms’ abilities to profit from the work they have, with 37 percent reporting they have been unsuccessful in passing those added costs onto project owners.

“Construction material prices are weighing heavily on construction starts,” added Richard Branch, Chief Economist for Dodge Data & Analytics in an Aug. 18 statement. “Lumber and copper prices have fallen in recent weeks; however, steel, plastic and other construction-related products are continuing their ascent. These increases will continue to impact construction starts over the coming months, somewhat muting the impact of stronger economic activity."

As a result of the supply chain challenges, more than half of firms report having projects canceled, postponed or scaled back due to increasing costs, noted the Autodesk-AGC survey. Twenty-six percent of firms report their projects have been delayed or canceled because of lengthening or uncertain completion times and 22 percent say changing market conditions have led to project delays or cancellations.

These challenging market conditions are a key reason why 26 percent of respondents expect it will take more than six months for their firm’s revenue to match or exceed year-earlier levels. And 17 percent are unsure when to expect a return to previous demand levels, added AGC.

Despite these challenges, contractors report as much difficulty filling positions as they experienced before the pandemic. Eighty-nine percent of firms that are seeking to fill hourly craft positions report having a hard time doing so. And 86 percent of firms seeking to fill salaried positions are also having a hard time hiring, according to the survey.

There are two main reasons so many firms report having trouble finding workers to hire, Simonson explained. The first is that 72 percent of firms say available candidates are not qualified to work in the industry due to a lack of skills, failure to pass a drug test, etc. The lack of qualified candidates affects union and open-shop firms almost equally: Some 70 percent of firms that always use union craft workers exclusively and 74 percent of open-shop firms report a lack of qualified candidates. And 58 percent of respondents report that unemployment insurance supplements are keeping workers away, according to AGC.

As a result of these shortages, almost one-third of firms report they have increased spending on training and professional development. Most firms, 73 percent, report they have increased base pay rates during the past year. And just over one-third of firms have also provided hiring bonuses or incentives during the past year, the survey found.

##########

Indeed, there does appear to be plenty of new work in the pipeline.

Last month, the Architecture Billings Index (ABI) recorded its sixth consecutive positive month, according to an Aug. 18 report from the American Institute of Architects (AIA). The ABI score for July was 54.6, slightly down from June’s score of 57.1. it still indicates very strong business conditions overall (any score above 50 indicates an increase in billings from the prior month). Scoring for new project inquiries also declined in July, but remained near its all-time high at 65.0. The score for new design contracts was essentially unchanged from June to July with a score of 58.0.

“In prior business cycles, architecture firms generally saw their project work soften quickly and then recover slowly,” said AIA Chief Economist, Kermit Baker, Hon. AIA, PhD. “So the strength of this recovery is unprecedented. Firm leaders who have leaned into this economic upturn by reinvesting in their firms by hiring staff and upgrading their technology, will likely have a better year than those that anticipated a slower recovery.”

Even so, it remains a grim reality that the Coronavirus pandemic is not yet over.

"A further risk to our sector is the rising number of COVID-19 cases due to the Delta variant," said Branch last month. "While we don’t expect significant business restrictions in response, it is a risk that cannot be fully discounted. On the upside, projects entering the planning stage remain at levels not seen in several years and forward progress on an infrastructure program and the federal budget provides hope that brighter days are ahead.”

##########

[UPDATE]

On Sept. 8, Dodge Data & Analytics released its latest Dodge Momentum Index, which dropped 3% in August to 148.7 (2000=100) from the revised July reading of 154.0. DMI is a monthly measure of the first (or initial) report for nonresidential building projects in planning, which have been shown to lead construction spending for nonresidential buildings by a full year.

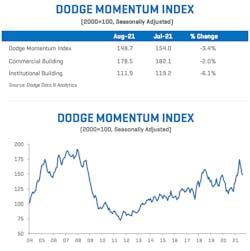

The commercial planning component lost 2% in August, while the institutional component fell by 6%. Projects entering the earliest stages of planning have declined following the torrid pace set in the spring. The decline in August was the third consecutive drop in the Momentum Index, which is now off 14% from the most recent high in May.

Since May the commercial component is down 10% and the institutional component is 22% lower. This reversal comes as prices for materials used in nonresidential buildings increase in combination with a shortage of labor and a rising number of new COVID-19 cases from the Delta variant, all working in concert to undermine confidence in the fledgling construction recovery. There were some pockets of strength in August, however, as more data center, education and warehouse projects moved into planning relative to the prior month. Additionally, the overall level of the Momentum Index is 19% higher than one year ago; institutional planning was up 17% and commercial planning was 20% higher than last year.

"Despite the recent declines in the DMI, it is still too early to call this a retrenchment or a new cyclical downturn," said Branch. "Demand for nonresidential buildings remains weak, but the recent rising number of new COVID cases should not cause the same amount of disruption as previous waves did. As the economy continues to trudge forward, momentum will return to the construction sector and moderate growth in projects entering planning will return."

##########

About the Author

Rob McManamy

Editor in Chief

An industry reporter and editor since 1987, McManamy joined HPAC Engineering in September 2017, after three years with BuiltWorlds.com, a Chicago-based media startup focused on tech innovation in the built environment. He has been covering design and construction issues for more than 30 years, having started at Engineering News-Record (ENR) in New York, before becoming its Midwest Bureau Chief in 1990. In 1998, McManamy was named Editor-in-Chief of Design-Build magazine, where he served for four years. He subsequently worked as an editor and freelance writer for Building Design + Construction and Public Works magazines.

A native of Bronx, NY, he is a graduate of both the University of Virginia, and The John Marshall Law School in Chicago.

Contact him at [email protected].