Economic Growth, Stability Now Tantalizingly Within Reach

Forecast season returned in full force this winter, buffeted by a maelstrom of new and continuing challenges, from inflation spikes and supply chain woes to political divisions and labor shortages. Oh, and of course, we can't forget the 800-lb gorilla in the mix, our terrible two-year-old Coronavirus pandemic -- set to start its third year this March -- along with the manifold health and safety concerns it continues to generate.

Factoring ALL of that into the many predictions for 2022, the prevailing mood of major economists who follow U.S. design and construction closely is surprisingly positive, as reflected in the latest American Institute of Architects (AIA) Consensus Construction Forecast, released January 19.

"The market is expected to see a healthy rebound, with spending increasing by 5.4% this year before accelerating to an additional 6.1% increase next year," said AIA Chief Economist Kermit Baker, PhD. “Architecture is one of the few industries where payrolls have already surpassed their pre-pandemic high, so meeting future staffing needs is a challenge that most firms will need to confront."

A quality problem to have, of course, and one that still bodes well for new projects across the board.

“Construction remained resilient and persistent throughout the year in the face of these difficult issues," added Richard Branch, chief economist for Dodge Construction Network. "While these challenges will remain in 2022, the industry is well-positioned to make further gains fed by a growing pipeline of nonresidential projects waiting to break ground and the infusion of money directed towards infrastructure."

- To see the interactive chart with individual forecasts, click here.

Specifically, the Consensus Forecast is most optimistic this year for industrial and manufacturing construction, which it expects to climb 9.4% in both 2022 and then by another 8.4% in 2023. Individual forecasts vary widely in specific categories, however. For instance, just in the industrial category, Moody's Analytics is predicting a very strong, 29.4% surge this year, while FMI Corp. is forecasting a 12.2% increase. On the flip side, Dodge actually expects manufacturing projects to dip by 3.5% in 2022, before bouncing back in 2023 with a rise of nearly 9%.

For its part, Dodge's forecast for 2022 is particularly bullish on commercial construction (+16.5%), hotels (+17%) and office buildings (+11.5%). Overall, it expects nonresidential construction to climb by 9.9% in 2022. Describing 2021 as "the rollercoaster year that changed construction forever," Dodge President and CEO Dan McCarthy noted, "The past year has taken the construction industry through hills and valleys — and the waves may well remain for the foreseeable future. The data continues to anticipate a healthy level of construction in 2022... (But) construction teams will not be free of the challenges of 2021: high material costs, unpredictable supply issues, aging construction labor force, volatile weather patterns, rapid adoption of new innovations transforming how we design, source and build things."

Painfully aware of all such mitigating factors, our industry's largest trade groups remain upbeat about prospects both near term and long term. But they are under no illusions.

“Contractors are, overall, very optimistic about the outlook for the construction industry in 2022,” said Stephen E. Sandherr, chief executive officer for Associated General Contractors of America (AGC). “While contractors face challenges this year, most of those will be centered on the need to keep pace with growing demand for construction projects.”

“The last two years have become increasingly unpredictable, due in large part to the coronavirus and public officials’ varied reactions to it,” added AGC chief economist Ken Simonson. “But, assuming current trends hold, 2022 should be a relatively strong year for the construction industry.”

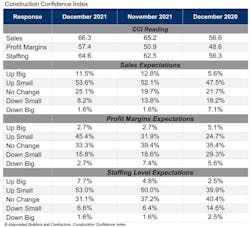

On Jan. 11, Associated Builders and Contractors released its latest Construction Confidence Index (CCI), based on a member survey conducted in late December. The new CCI readings for sales, profit margins and staffing levels all increased in December, indicating expectations of growth over the next six months.

“Demand for construction services in America remains strong,” said ABC Chief Economist Anirban Basu. “Contractors have been upbeat about sales and employment prospects for months. What changed in December is that a growing fraction of contractors now believe that profit margins will rise during the next six months despite rising costs due to labor shortages and volatile materials prices."

ABC's Construction Backlog Indicator actually slipped a bit in December, but it still finished the year higher than the previous December. Firms in the Midwest and West also reported more activity for the year than their ABC counterparts in the Northeast and South.

“Backlog fell in the infrastructure category, but activity in that category is set to heat up in 2022 as federal infrastructure funds tied to the Infrastructure Investment and Jobs Act of 2021 (IIJA) begin to flow,” added Basu. “Backlog in the heavy industrial category also declined on a monthly basis, but over the past year backlog in this segment has climbed dramatically as manufacturers attempt to address goods shortages and more CEOs consider bringing some of their supply chains back to America. Industry backlog could be negatively impacted by elevated steel and other materials prices, with some projects cancelled and others redesigned to shift away from intense steel use.”

"Despite it all, our economy’s ability to overcome the pandemic has been admirable," said Moody's chief economist Mark Zandi, writing in his own new report, Time to Heal. "If everything sticks roughly to our baseline script, it will have taken less than three years for the economy to fully recover from that first blow of the pandemic. It took a decade for the economy to recover from the global financial crisis. This is testament to the dedication of our healthcare providers and other frontline workers; the ingenuity of our pharmaceutical industry and medical technology; the massive collective response of federal, state and local governments; and the resilience of the American economy and people."

A welcome perspective, indeed. Our industry may not be out of the woods yet, of course. But after all that we have been through these last 22 months, it is well worth reminding ourselves that, sometimes, there is victory in just still being in the game.

##########

About the Author

Rob McManamy

Editor in Chief

An industry reporter and editor since 1987, McManamy joined HPAC Engineering in September 2017, after three years with BuiltWorlds.com, a Chicago-based media startup focused on tech innovation in the built environment. He has been covering design and construction issues for more than 30 years, having started at Engineering News-Record (ENR) in New York, before becoming its Midwest Bureau Chief in 1990. In 1998, McManamy was named Editor-in-Chief of Design-Build magazine, where he served for four years. He subsequently worked as an editor and freelance writer for Building Design + Construction and Public Works magazines.

A native of Bronx, NY, he is a graduate of both the University of Virginia, and The John Marshall Law School in Chicago.

Contact him at [email protected].