Resurgent Economy Now Adds European War to Growing Concerns

By ROB McMANAMY, HPAC Engineering

As the U.S. marks two years since the pandemic shut down life worldwide, our industry's collective desire for 'normalcy' now finds itself confronted by yet another anxiety-inducing challenge — an actual 'hot war' in Europe, with the potential for a nuclear standoff.

So, 'normalcy' remains on hold.

Already dealing with runaway inflation not seen since the first Reagan Administration, the U.S. now faces additional price escalation sure to follow the Biden Administration's March 8 announcement banning the import of Russian oil and liquified natural gas (LNG). That, of course, was just the latest in a growing package of punitive economic sanctions that the European Union and members of the North Atlantic Treaty Organization (NATO) have imposed on Russia since it invaded Ukraine on Feb. 24.

With hundreds already dead in Ukraine and no negotiated peace in sight, growing tensions in Europe have manifested themselves most clearly in the U.S. in the form of sky-rocketing fuel costs. And this comes on the heels of already rising materials prices tied to continuing global supply chain woes. "There are indications that supply chain issues have improved slightly, though the Ukraine/Russia war may create new issues on that front," said Anirban Basu, chief economist for Associated Builders and Contractors (ABC).

"Certainly with fuel prices at the pump, we're feeling some of the impact of the war in Ukraine. But, of course, nothing like what the people of Ukraine are feeling, or the surrounding countries, who are seeing two million refugees," noted Ken Simonson, chief economist for Associated General Contractors of America (AGC). Speaking on a March 9 podcast with Pit & Quarry, he added, "The construction industry is a huge user of diesel fuel, so we are quite sensitive to what happens to oil prices in various forms. We had thought that last year and 2020 had had a lot of volatility, with incredible prices swings on lumber, and steel, too... But that volatility now seems likely to be even more extreme this year with oil prices, for sure, but also for other prices, as energy costs are factored in."

Economist Brian Beaulieu is CEO of ITR Economics, and a frequent forecaster for the American Boiler Manufacturers Association. He spoke at ABMA's annual meeting earlier this year. On March 11, while acknowledging the human tragedy still unfolding in Ukraine, Beaulieu posted these otherwise reassuring comments on his blog:

Keep in mind that we entered this morass in good shape economically:

- After-tax incomes are up (relative to pre-COVID);

- Personal savings are at a post-Great-Recession normal level;

- Jobs are plentiful;

- Debt service levels as a percentage of Disposable Personal Income are low;

- Businesses' liquidity is high;

- Profits are up;

- Money is cheap (in both nominal and real-dollar terms).

The Consumer Price Index and commodity prices in general were in the early stages of shifting from ascent into lower rates of inflation and modest price decline, respectively, before Russia invaded. The war has clearly disrupted the normal course of economics. This is not unusual; indeed, it is normal for a war to do this. What is also normal is that after the war, the economic trends will once again prevail. That means disinflation essentially across the board and lower gasoline, diesel, heating oil, and propane prices (although not necessarily back to pre-war levels).

Nobel Prize-winning economist Paul Krugman is calling the war's economic impact "the Putin shock." On March 8, he wrote in The New York Times, "It will be bad, but not catastrophic. Specifically, the Putin shock seems unlikely to be nearly as bad as the oil shocks that roiled the world economy in the 1970s."

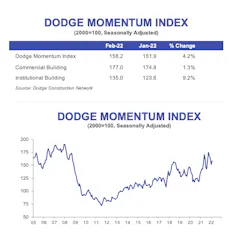

Also on March 8, Dodge Construction Network (DCN) released it latest Dodge Momentum Index, which recorded a 4% increase for the month of February. That broke a string of three consecutive monthly declines that had followed the Index's 14-year high reached in October 2021. Much of February’s gain was due to a 9% jump in the institutional component, as more education and healthcare projects entered planning. Commerical planning remained solid thanks to office and warehouse projects. When compared to February 2021, the overall Momentum Index was 11% higher in February 2022.

"It is certainly reassuring that the pipeline of projects awaiting start continues to grow, especially in light of continuing pricing pressures, as it relates to materials prices, of course, as well as a labor scarcity," noted Richard Branch, DCN Chief Economist. "But the bigger question here is this increase sustainable in the face of what will likely be continuing upward pressure on material prices due to the conflict in Ukraine? As we look at the timing gap between when a project enters pre-design and when it breaks ground, that 'lag-to-start', as we call it, is now nine months longer than it was before the pandemic. It's very likely now that we will see that gap grow over the coming months. What that means in terms of the Momentum Index is that all those projects that have been entering planning over the past few months will have a greater impact toward the end of 2022 and into early 2023."

In the meantime, owners, architects, engineers, contractors and subcontractors all must wrestle with wildly fluctuating costs.

“Architecture billings, while remaining at very healthy levels in recent months, have slowed considerably from the middle of last year,” noted AIA Chief Economist, Kermit Baker, PhD, in late February. “This no doubt reflects delays in the construction sector caused by supply challenges for both labor and materials, as well as ongoing staffing constraints at architecture firms,” he added.

“Construction firms are going to have to pass along the rising materials prices to remain successful,” said AGC CEO Stephen E. Sandherr on March 14. “And firms should not be punished for failing to foresee a Russian invasion, spiking oil prices and soaring inflation when preparing public works bids.”

Toward that end, AGC officials urged anyone procuring construction services — both public and private owners — to look for ways to help contractors offset losses from spiking materials prices on existing projects, ideally via more flexible, revised contracts.

Construction employment still growing

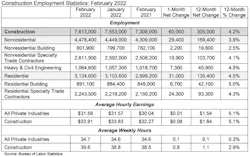

Costs aside, construction employment has continued to climb this year, adding 60,000 jobs between January and February, according tie the latest monthly data from the U.S. Bureau of Labor Statistics (BLS). Hourly pay also rose at the steepest pace in nearly 40 years, noted AGC, which is now lobbying for more federal aid to boost career training and technical education in the industry.

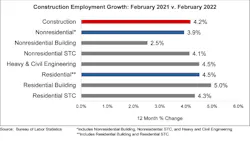

“All segments of construction added workers in February,” said Simonson. “However, filling positions remains a struggle, as pay is rising even faster in other sectors.”

Average hourly earnings for “production and nonsupervisory employees”—largely, hourly craft workers, in the case of construction—increased 6% from February 2021 to last month. That was the steepest 12-month increase since December 1982, Simonson noted.

The industry average of $31.62 per hour for such workers exceeded the private sector average by 17%, he added. Overall, employment rose at all types of construction firms in February. Nonresidential construction firms added 29,400 employees. That included 19,900 more employees among specialty trade contractors, 7,300 at heavy and civil engineering construction firms, and 2,200 working for general building contractors.

Sandherr said it is clear the industry will need to hire hundreds of thousands of additional workers in each of the next several years to complete projects that will be funded by the recently enacted Bipartisan Infrastructure law, as well as to satisfy the continuing demand for homebuilding and private nonresidential structures. He urged Congress and the Biden Administration to increase funding for career and technical education and to support a wider range of apprenticeship and training opportunities.

“Bottom line: The U.S. economy is charging into the post-pandemic world with significant momentum, and nonresidential construction is part of that story,” said ABC's Basu. “At the heart of America’s economic momentum is rapid workforce growth, with more people re-entering the workforce to take advantage of higher wages and to better contend with rapidly rising prices... With demand strong and the supply side of the economy in repair, 2022 is setting up to be a strong year for contractors," he added.

“But there remain many reasons for concern,” noted Basu.

Not the least of which is a deadly geopolitical conflict that continues to roil world markets daily.

##########

About the Author

Rob McManamy

Editor in Chief

An industry reporter and editor since 1987, McManamy joined HPAC Engineering in September 2017, after three years with BuiltWorlds.com, a Chicago-based media startup focused on tech innovation in the built environment. He has been covering design and construction issues for more than 30 years, having started at Engineering News-Record (ENR) in New York, before becoming its Midwest Bureau Chief in 1990. In 1998, McManamy was named Editor-in-Chief of Design-Build magazine, where he served for four years. He subsequently worked as an editor and freelance writer for Building Design + Construction and Public Works magazines.

A native of Bronx, NY, he is a graduate of both the University of Virginia, and The John Marshall Law School in Chicago.

Contact him at [email protected].