Market Momentum Still Strong, Despite Conflicting Measures

Everybody wants a bull market. Certainly, no one wants a bear market. But lest we forget, a charging bull can also be quite erratic. And, well, it has horns. So, remember to watch out for them, too.

This spring, headlines have seemed to alternate daily from good news to bad, and then back again.

Record high inflation? That's been countered by record low unemployment. Materials shortages caused by global supply chain woes? That's been balanced by continuing growth in project backlogs. Contractor confidence ebbing? That's been offset by rising designer optimism. Global economic cycles ready to break free of COVID-19? Maybe, but international supply chains are now being disrupted by a government-imposed shutdown of Shanghai to head off a resurgence of the Coronavirus. Sound familiar?

Toss in the ongoing war in Europe between Russia and NATO-backed Ukraine, and we are left with a world economy that is still straining to roar after a prolonged pandemic pause. But it is unsure how to proceed with so many new hurdles in the way.

With that in mind, on April 19, the International Monetary Fund (IMF) revised downward its 2022 economic forecast with this statement:

The war in Ukraine has triggered a costly humanitarian crisis that demands a peaceful resolution. At the same time, economic damage from the conflict will contribute to a significant slowdown in global growth in 2022 and add to inflation. Fuel and food prices have increased rapidly, hitting vulnerable populations in low-income countries hardest. Global growth is projected to slow from an estimated 6.1% in 2021 to 3.6% in 2022 and 2023. This is 0.8 and 0.2 percentage points lower for 2022 and 2023, respectively, than projected in January... War-induced commodity price increases and broadening price pressures have led to 2022 inflation projections of 5.7% in advanced economies and 8.7% in emerging market and developing economies—1.8 and 2.8 percentage points higher than projected last January. Multilateral efforts to respond to the humanitarian crisis, prevent further economic fragmentation, maintain global liquidity, manage debt distress, tackle climate change, and end the pandemic are essential.

In an accompanying press briefing that day in Washington DC, IMF Chief Economist Pierre-Olivier Gourinchas explained, "The war adds to the series of supply shocks that have struck the global economy in recent years. Like seismic waves, its effects will propagate far and wide—through commodity markets, trade, and financial linkages."

And that, of course, includes design and construction.

"The Russia-Ukraine war has exacerbated inflationary pressures and will likely result in more aggressive monetary tightening by the Federal Reserve (which meets again in early May)," noted Anirban Basu, chief economist for Associated Builders and Contractors (ABC). "For now, the average contractor expects to be able to pass along a significant fraction of the cost increases to project owners. It remains to be seen whether that will persist as interest rates rise.”

On April 19, the Dodge Construction Network reported a 12% drop in March construction starts, to a seasonally adjusted annual rate of $903.8 billion. DCN noted, however, that the value of three large manufacturing facilities begun in February had inflated the prior month's tally. As a result, nonresidential building starts technically fell 29% in March. But if the three large projects are removed, nonresidential starts in March would have actually risen 10%.

Overall, the first-quarter data was positive. Year-to-date, total construction was 9% higher in the first three months of 2022 than in the same period of 2021, DCN said. For the 12 months ending March 2022, nonresidential building starts were 25% higher than in the 12 months ending March 2021. Commercial starts were up 21%, while institutional starts rose 12%, and manufacturing starts soared 162% on a 12-month rolling sum basis. By any measure, a remarkable climb from the depth of the pandemic.

“The volatility caused by the ebb and flow of large projects masks an underlying trend of strengthening in construction starts,” stated Richard Branch, DCN chief economist. “Nonresidential construction has benefited from the growing confidence that the worst of the pandemic is in the rear-view window. The pipeline of projects waiting to start continues to fill, suggesting this trend will continue. However, higher prices and a shortage of skilled labor will slow the progress of those projects through the design and bidding stages, resulting in moderate growth in starts activity.”

All Rise: Design billings, construction employment up

The American Institute of Architects (AIA) released its latest Architectural Billings Index (ABI) score on April 20, which recorded a sharp increase in March to 58.0, up from a score of 51.3 in February. (Any ABI score above 50 indicates an increase in billings.) During March, scoring for both new project inquiries and design contracts expanded, posting scores of 63.9 and 60.5, respectively, AIA noted.

“The spike in firm billings in March may reflect a desire to beat the continued interest rate hikes expected in the coming months,” said AIA Chief Economist, Kermit Baker, Hon. AIA, PhD. “However, since project backlogs at architecture firms have reached seven months, a new all-time high, it appears that firms are having a difficult time keeping up with this uptick in demand for design services.”

Baker noted that the latest ABI score of 58.0 for March is one of the highest scores seen since the economic recovery began just over a year ago. Despite ongoing concerns about rising inflation and the war in Ukraine, business conditions remained robust at most architecture firms, he added. Indicators of future work strengthened this month as well, most notably with the value of new design contracts, which also saw strong growth. In addition, design firms reported that at the end of the first quarter of 2022, their respective backlogs stood at an average of 7.2 months.

"This was an increase of more than a month from one year ago and a new all-time high since we began collecting data on backlogs in 2010," he said. "Looking at design contracts and backlogs together indicates that most firms have plenty of projects in the pipeline to keep them busy over the coming months, although finding enough employees to complete these projects remains challenging."

Indeed, industry hiring for design and construction has been surging, straining to keep up with demand.

Construction employment climbed by 19,000 jobs between February and March, while spending on construction projects rose for the 12th consecutive month in February, according to recent data from the Bureau of Labor Statistics (BLS) and the U.S. Census Bureau. Between March 2021 and March 2022, industry job growth increased in three-fourths of U.S. metro areas, according to an analysis of that data done by the Associated General Contractors of America (AGC). Labor shortages likely kept many firms from adding even more workers during the past year, said AGC Chief Economist Ken Simonson.

“It is heartening to see construction employment come back from the depths of pandemic-induced job losses in most areas,” he added. “But the skyrocketing number of job openings shows the industry needs far more workers than are available in many parts of the country.”

AGC leaders warned that further gains may stall unless the supply of workers and materials improves. They urged federal officials to end tariffs on key materials and broaden training and education opportunities for construction careers.

“Construction is contributing significantly to the expansion of employment and the overall economy,” noted Simonson. "But the sector is facing growing challenges in terms of filling job openings, obtaining materials, and keeping up with soaring wages and prices.”

Industry employment totaled 7,628,000 in March, topping the pre-pandemic peak set in February 2020 for the first time. Residential building and specialty trade contractors added 7,600 employees in March, and the sector’s employment exceeded the February 2020 level by 161,000 or 5.4%. Despite the recent employment increases, however, construction job openings at the end of February totaled 364,000, the largest February total, by far, in the 22-year history of that series, Simonson noted. Openings exceeded the 342,000 workers hired in February, implying that contractors wanted to hire more than twice as many workers as they were able to, he added.

Association officials said the industry will need to obtain materials on a more timely basis and hire hundreds of thousands of additional workers in order to execute projects that will soon be funded by the Bipartisan Infrastructure law, on top of the continuing demand for homebuilding and private nonresidential structures. AGC also urged Congress and the Biden Administration to end lumber, steel, and other tariffs, increase funds for career and technical education, and support a wider range of apprenticeship and training opportunities.

“Contractors are doing their part to add employees and complete projects,” said Stephen E. Sandherr, AGC's chief executive officer. “But there won’t be enough materials or workers to go around if officials in Washington fail to allow more goods into the U.S. and prepare more jobseekers for these opportunities.”

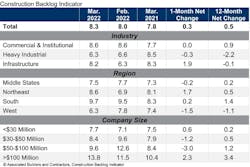

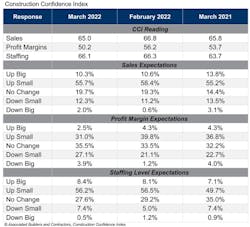

Reflecting that concern among its own members, ABC released the results of its latest member survey on April 12. Conducted between March 22 and April 5, the national survey found that ABC's Construction Backlog Indicator had increased to 8.3 months in March, up 0.5 months from March 2021. At the same time, however, the association's Construction Confidence Index readings for sales, profit margins and staffing levels declined in March. All three measures remain above the threshold of 50, however, indicating expectations of growth over the next six months.

“Demand for construction services remains strong despite sky-high materials prices, skills shortages and elevated bids,” said ABC's Basu. “ABC contractors indicate that demand will remain strong, with 65% expecting sales to grow over the next six months. Backlog increased in March, indicating that bidding opportunities remain plentiful. The recent rise in interest rates could induce certain project owners to move forward with construction work to access affordable investment capital while it remains available. It is also conceivable that at some point private demand for construction services will decline as the cost of capital rises."

But while demand is good, supply is now not assured, he added.

“More than three-quarters of contractors indicate that they had recently suffered some setback in delivering construction services," Basu noted. “Among the primary factors are a lack of sufficiently skilled workers as well as materials and equipment shortages. These dynamics will continue to increase the cost of construction delivery during the months to come."

Which brings us back to our ongoing record inflation and the whip-saw effect it is having on our national push-me/pull-you economic recovery. Add to that the latest chaos caused this month by the recent controversial ruling of a federal judge in Florida, striking down the CDC's authority to impose public health mask mandates on federal agencies... No wonder the Wall Street bull seems spooked.

For the moment, though, let us pause and remember that even this spring's skittish bull is still preferable to the ravenous and unwelcome bear that upended our businesses and was still devouring jobs and profits just 18 months ago.

About the Author

Rob McManamy

Editor in Chief

An industry reporter and editor since 1987, McManamy joined HPAC Engineering in September 2017, after three years with BuiltWorlds.com, a Chicago-based media startup focused on tech innovation in the built environment. He has been covering design and construction issues for more than 30 years, having started at Engineering News-Record (ENR) in New York, before becoming its Midwest Bureau Chief in 1990. In 1998, McManamy was named Editor-in-Chief of Design-Build magazine, where he served for four years. He subsequently worked as an editor and freelance writer for Building Design + Construction and Public Works magazines.

A native of Bronx, NY, he is a graduate of both the University of Virginia, and The John Marshall Law School in Chicago.

Contact him at [email protected].