Is it possible that the long-predicted economic recession that we have all been bracing for has somehow missed us?

Could it be that the prevailing doom and gloom over inflation that first started gathering after the Federal Reserve began raising interest rates in March 2022 has actually come and gone?

Well, maybe so. After all, the Federal Reserve announced June 14 that it was "pausing" its campaign of 10 consecutive rate hikes, although Chair Jerome Powell reserved the right to resume increases later this summer. Even so, there was an inescapable feel in general this month that the real storm may have passed.

"People have been using the wrong R-word to describe the economy," said Joe Brusuelas, chief economist at RSM, in a recent interview with CBS MoneyWatch. "It's resilience — not recession."

“This time is different,” added Mark Zandi, Moody’s Analytics chief economist, in a June 20 op-ed for CNN.com. “Yes, the economy is fragile and vulnerable to losing the script. And goodness knows we have been off script more often than not in recent years. But odds are that we will buck history and avoid recession.”

Indeed, that is what the latest construction data indicates, too, buoyed by still-strong project backlogs and record hiring. Elevated levels of state and federal infrastructure spending, of course, continue to bring stability.

“Public dollars are flooding into the manufacturing and infrastructure sectors, leading to significant growth over the last year," noted Richard Branch, chief economist for the Dodge Construction Network. "(But) the mostly private sectors of the building market like offices, multifamily and retail are struggling under the weight of higher interest rates, tightening lending standards and declining demand. The second half of the year is shaping up to be a challenging one.”

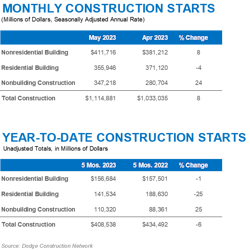

Even so, Dodge reported on June 20 that nonresidential building starts rose 8% in May to a seasonally adjusted annual rate of $412 billion. The driving force behind the increase was manufacturing starts, which more than doubled over the previous month. Commercial starts tumbled 20% in May due to a sharp pullback in office and retail starts, while hotel starts moved higher. Institutional starts fell just 1% in May with education starts falling, but healthcare increasing, according to Dodge.

Meanwhile, business conditions at architecture firms bounced back in May, following a modest downturn in April, according to the latest data from the American Institute of Architects (AIA), released June 21. The AIA/Deltek Architecture Billings Index (ABI) score for May was 51.0, the highest it has been since last September.

In addition, inquiries into new projects and the value of new design contracts also bounced back this month, with inquiries reaching their highest level in nine months, and design contracts increasing for the first time since February. "With recent declines in inflation and a pause in interest rate increases, it appears that the economy may be stabilizing," wrote AIA Chief Economist Kermit Baker, Hon. AIA, PhD. “The modest improvement in overall demand for architectural services that we saw last month is encouraging news."

AIA cited some feedback from members in its monthly ABI report. Two comments:

- “Although monthly billings and new design [contract] values are both up for the past month, things appear to be softening. Our pipeline is not replenishing at the rate it was, and solid production projects are more rare. The second half of 2023 is of some concern”— said one designer at a 19-person firm in the South that specializes in commercial/industrial work;

- “The work is still out there, it’s just taking more effort to get the work. We are seeing our repeat clients slow down decision making, and moving projects forward, requiring us to go find new clients”— added a representative of a 22-person firm in the West, specializing in residential work.

Significantly, AIA also noted that construction employment had strengthened last month, adding 25,000 new jobs. And architectural services employment added an additional 1,100 new positions in April (the most recent data available), the largest monthly gain so far this year, bringing industry employment to a new post-pandemic high.

Overall, construction employment in May was up in 42 states and the District of Columbia from a year earlier. Those numbers increased last month in 24 states, according to new data released earlier this month by the Bureau of Labor Statistics.

“Contractors remain busy nationwide, with bulging order books for future work,” said Ken Simonson, chief economist for Associated General Contractors of America (AGC). “But they are having trouble filling job openings when the industry unemployment rate is only 3.5%. That probably accounts for the recent lack of job gains in many states.”

For its part, Associated Builders and Contractors (ABC) reported June 13 that its latest Construction Backlog Indicator (CBI) remained at 8.9 months in May, according to an ABC member survey conducted May 20 to June 7. That reading is just 0.1 months lower than what the survey recorded in May 2022.

"At nearly nine months, backlog is essentially unchanged from a year ago," noted ABC Chief Economist Anirban Basu. “During a period of ongoing tumult associated with major bank failures, a near-miss debt ceiling crisis and shifting monetary policy, nonresidential construction backlog has remained remarkably stable.”

All in all, the economy's spring report card was remarkably strong, especially for the AEC industry. And now that May's potentially disastrous flirtation with federal financial default has been resolved for at least two years, it may actually be time to exhale again.

Indeed, there is plenty of work to do this summer, and plenty of funding available to keep us all busy well into 2024. With that in mind, it is conceivable that infrastructure projects can continue to lead until such time as other building markets are ready to rebound.

##########

About the Author

Rob McManamy

Editor in Chief

An industry reporter and editor since 1987, McManamy joined HPAC Engineering in September 2017, after three years with BuiltWorlds.com, a Chicago-based media startup focused on tech innovation in the built environment. He has been covering design and construction issues for more than 30 years, having started at Engineering News-Record (ENR) in New York, before becoming its Midwest Bureau Chief in 1990. In 1998, McManamy was named Editor-in-Chief of Design-Build magazine, where he served for four years. He subsequently worked as an editor and freelance writer for Building Design + Construction and Public Works magazines.

A native of Bronx, NY, he is a graduate of both the University of Virginia, and The John Marshall Law School in Chicago.

Contact him at [email protected].