Soft Landing More Likely, Industry Confidence Strong

After nearly a year of doom and gloom, with many fearing recession around every corner, and the Federal Reserve Bank seemingly obsessed with taming inflation —no matter the cost— the U.S. economy still has not succumbed.

On the contrary, as AEC firms this fall start focusing more attention on 2024 planning and industry analysts prepare their forecasts for later this year, the darkest clouds appear to have lifted. (Provided the U.S. can avoid a budget stalemate and government shutdown in October, of course.)

"Almost all the available evidence suggests that the U.S. economy is achieving what many economists had thought impossible — a soft landing in which inflation returns to acceptable levels without a recession," said economist Paul Krugman on Sept. 15.

- Total U.S. construction starts climbed 6% in August. Read more here.

Three days earlier, Anirban Basu, chief economist for Associated Builders and Contractors (ABC) gave his own assessment. “There’s no sign of a construction recession in the near term. If anything, contractors are more upbeat, as policy and technology shifts along with economic transformation, are creating substantial demand for improvements and growth in America’s built environment."

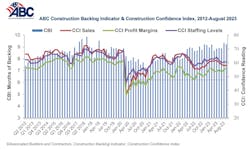

Basu made his comments after ABC released its latest monthly Construction Backlog Indicator (CBI), which declined slightly to 9.2 months in August. The measure was down just 0.1 month, according to an ABC member survey conducted between Aug. 21 and Sept. 6. Still, the reading is 0.5 months above the August 2022 level.

“Backlog continues to be at the upper end of historic levels, with the infrastructure category registering substantial gains in backlog in August," Basu noted. "That suggests that a growing number of public works projects is poised to break ground.”

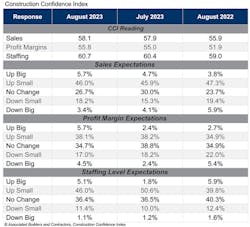

ABC’s Construction Confidence Index (CCI) reading for sales, profit margins and staffing levels moved higher in August. All three readings remained above the threshold of 50, indicating expectations of growth over the next six months.

“While a plurality of contractors expects only small improvements in sales, profit margins and staffing over the next six months, even incremental improvement is remarkable in the context of tightening credit, higher project financing costs and lingering fears of recession,” added Basu.

Inflation Down, But Still Concerning

Financing costs, of course, mean interest rates, and the Federal Reserve Bank has spent the last 18 months raising those rates 11 times, from near zero in March 2022 to 5.5% this July. The goal, of course, has been to bring the U.S. core inflation rate down to 2.0%. As a result, inflation has dropped from a post-pandemic high of 8.5% early last year to 3.2% last month.

Despite that relatively rapid progress, however, most still expect the Fed to raise interest rates again in late September.

Speaking at the Fed's annual symposium Aug. 25 in Jackson Hole, WY, Fed Chairman Jerome Powell was poetically opaque.

"We are navigating by the stars under cloudy skies," he said. "At upcoming meetings, we will assess our progress based on the totality of the data and the evolving outlook and risks... Restoring price stability is essential to achieving both sides of our dual mandate. We will need price stability to achieve a sustained period of strong labor market conditions that benefit all... We will keep at it until the job is done," Powell concluded.

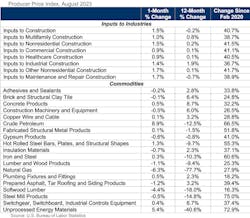

Looking specifically at the construction industry, the price of materials and services used in nonresidential construction increased 1.1% from July to August, driven by an extreme jump in diesel fuel costs, according to data from the U.S. Bureau of Labor Statistics (BLS), and analysis by Associated General Contractors of America (AGC).

“The steep climb in diesel prices since July is a reminder that construction cost worries have not gone away,” said AGC chief economist Ken Simonson on Sept. 14. “An even greater challenge for most contractors is finding enough qualified workers to complete the many projects available to work on.”

The producer price index (PPI) for diesel fuel, which covers the selling price at the terminal rack or refinery, soared 34.6% from mid-July to mid-August, the largest one-month jump since 1990. Simonson noted that retail diesel prices have continued rising since then and have climbed 77 cents per gallon in the past 10 weeks.

The 1.1% monthly increase in construction input costs was the largest since January, Simonson pointed out. In contrast, the index for new nonresidential building construction —a measure of the bid prices contractors said they would charge to erect a set of new structures— edged up just 0.2% in August. He noted that both indexes posted relatively mild year-over-year changes: 0.1% for inputs and 4.0% for bids.

Prices for most major construction inputs other than fuel were stable or declined in August. Indexes for cement and architectural coatings such as paint were flat. There were decreases of 0.2 percent in the index for plastic construction products, 0.5 percent steel mill products, and 0.4 percent for gypsum building materials.

##########

About the Author

Rob McManamy

Editor in Chief

An industry reporter and editor since 1987, McManamy joined HPAC Engineering in September 2017, after three years with BuiltWorlds.com, a Chicago-based media startup focused on tech innovation in the built environment. He has been covering design and construction issues for more than 30 years, having started at Engineering News-Record (ENR) in New York, before becoming its Midwest Bureau Chief in 1990. In 1998, McManamy was named Editor-in-Chief of Design-Build magazine, where he served for four years. He subsequently worked as an editor and freelance writer for Building Design + Construction and Public Works magazines.

A native of Bronx, NY, he is a graduate of both the University of Virginia, and The John Marshall Law School in Chicago.

Contact him at [email protected].